Payviders Are Already Impacting Health System Revenue Growth and Market Share

In recent years, insurers have ramped up acquisitions of providers and practices. Payers and private equity have scooped up 32,000 physicians since 2020 – an 86% increase.

In recent years, insurers have ramped up acquisitions of providers and practices. Payers and private equity have scooped up 32,000 physicians since 2020 – an 86% increase.

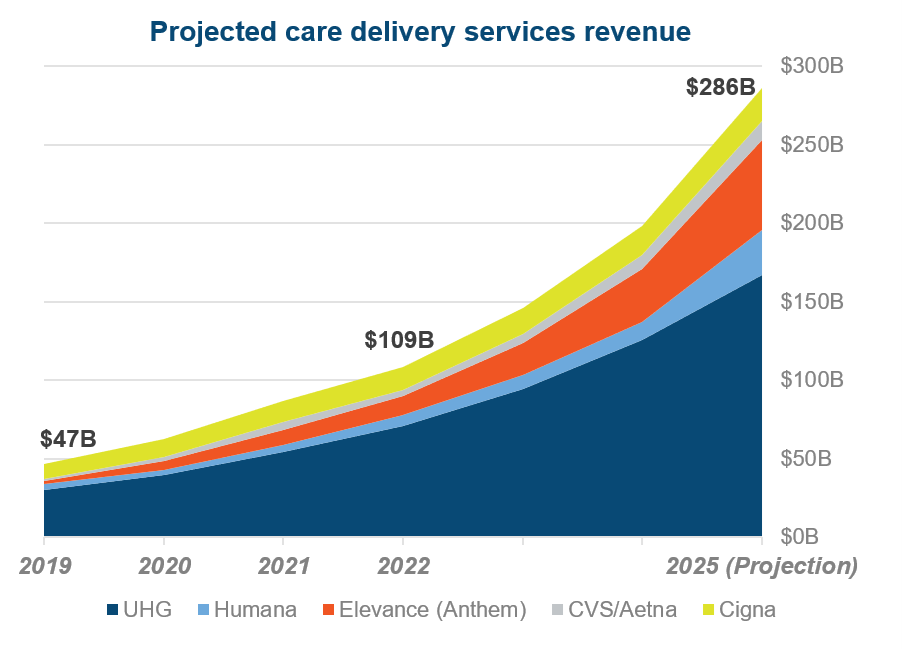

By evolving towards paying and delivering care, many payers are more accurately described as ‘payviders’. We anticipate that by 2025, the five largest payers will generate $286 billion in revenue from care delivery alone.

What is the immediate threat to health system revenue growth and market share? Here are three things you need to know about this new era:

1. Virtual-first plans are leveling the playing field, driven by pandemic demand.

Before the pandemic, only Humana operated a virtual-first plan. But across 2021 and 2022, essentially every payer launched a virtual primary care platform, cementing their role in care delivery.

What’s the benefit?

These plans give payers tremendous data, and it’s attractive for employers looking to offer lower-premium and zero co-pay options.

Most importantly, payviders like United Health Group (UHG)-Optum and CVS-Aetna can steer patients to their own urgent care centers for in-person care, cutting patient volume and referrals from leading health systems.

2. UHG’s Optum is the undisputed market-leader, and has defined the must-have assets for large payers to own.

As of 2022, Optum employs roughly 10% of all U.S. physicians, more than double the amount of Ascension and HCA.

UHG has flipped the model, viewing Optum as their front door to new patients.

To stay competitive, all large payers now must own a similar suite of assets. At minimum, this means a PBM and virtual care platform, and may yet include primary care, ASCs, and home-based care.

3. Optum’s early acquisitions have positioned them to siphon profitable care services.

Optum made several early acquisitions in care delivery that have proven highly profitable. In 2015, Optum purchased MedExpress urgent care for an undisclosed amount, and two years later paid $2.3 billion for Surgical Care Affiliates. UHG now aims to have 55% of its members receive outpatient surgeries at ASCs instead of traditional hospital-based, outpatient settings.

And although payviders have largely stayed away from acute care, Optum has entered direct partnerships with health systems to operate IT and revenue cycle operations. The latest of these partnerships is with Northern Light Health, where it’s projected to save the system $1B over 10 years.

The ‘So What?’ on Payviders for Health Systems

Payviders pose a few risks to leading health systems, but nothing more significant than the potential loss of patient volumes.

- First, payviders are directly competing for patients in non-acute care settings like virtual, primary, and urgent care.

- Second, payviders are stepping up their efforts to refer patients to non-leading health system care sites, or prevent the care altogether through at-home services.

Health system strategists must compete now before other payers grow as large as Optum. The winners may be those who disrupt themselves on cost of care to maintain payer relationships or double down on consumer-focused goals to hedge against being taken out of payers’ networks. Whichever path is chosen, the cost of inaction is too high.

Health system strategy leaders need fast, accurate, and unbiased market surveillance. Our Strategy Catalyst program provides trusted insights that strategy leaders rely on to quickly and expertly chart their course, leading transformative innovation to drive revenue growth while protecting market share. Learn more.