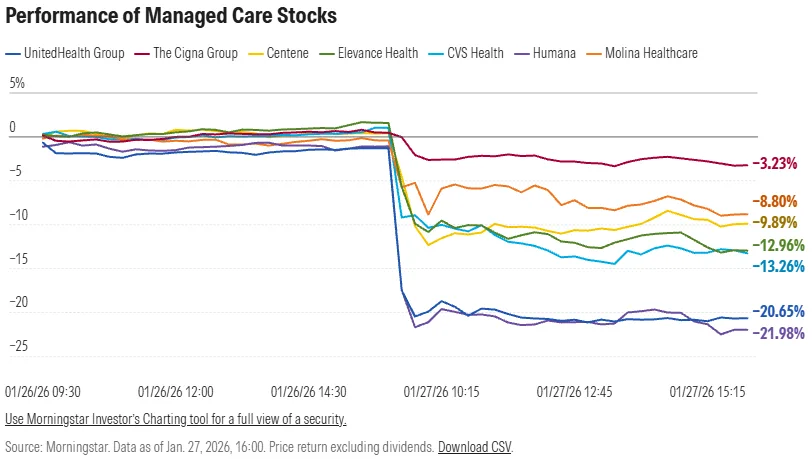

In late January, the stock prices of major MA-dependent payers like UnitedHealth and Humana plummeted more than 20% after CMS indicated it would increase overall MA rates by just 0.09% for the 2027 plan year.

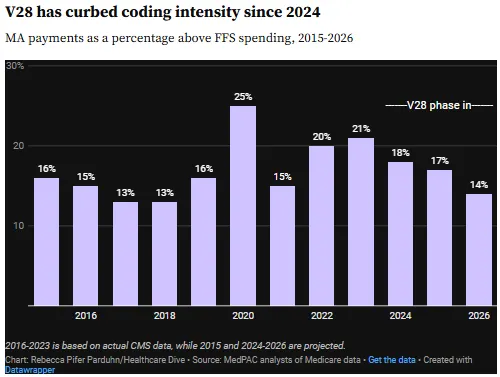

Major insurers and their lobbyists at AHIP and the Alliance of Community Health Plans warned that the effectively flat rate increase will lead to benefit cuts and cost increases, especially in light of rising healthcare utilization since the pandemic and falling reimbursement under the V28 risk adjustment model.

Along with the flat rate proposal, CMS is also proposing to exclude chart reviews that aren’t linked to actual medical care from MA risk adjustment. UnitedHealth’s prolific use of chart reviews to inflate payment rates attracted scrutiny from policymakers and the Justice Department. CMS projects that the change will save the federal government more than $7B in 2027 alone.

So What?

The announcement sent shockwaves through the market, but in many ways it’s a culmination of long-running concerns with MA: its rapid growth, its cost relative to traditional Medicare, and various ways that many of the largest carriers have gamed the system to maximize their reimbursement. Here’s our take on what it signals for the future of the program:

1. MA growth is forcing the Trump administration to choose between two priorities: cost containment and private sector solutions.

MA was created to bring private sector efficiency and flexibility to the Medicare program, but it has frequently faced claims that the federal government spends more per enrollee than traditional Medicare, after accounting for underlying health risk. High profits among MA insurers prior to 2021 only underscored the perception that the program has fat to cut. This arguably made the program a ripe target for the Trump administration’s agenda to cut healthcare spending and reorient the economy away from the sector more generally.

On the other hand, the program’s rapid growth has been a boon for proponents of greater private sector involvement in federal health programs—another major priority for this administration. If policymakers could be convinced that the flat rate proposal is jeopardizing the program’s continued growth, they might be persuaded to soften the blow. Typically, final MA rates come in around 1% higher than the initial proposal.

2. The major national payers are retreating from less profitable markets, joining an exodus by provider-sponsored plans.

UHG, Humana, and Aetna all project membership losses this year, and 2027 could be even steeper. Health systems including Michigan Medicine, Carle Health, and Ochsner Health have also recently discontinued their provider-sponsored plans. Recent market share winners picking up the slack have included regional nonprofits like SCAN Health (+40% membership growth YoY), BCBS affiliates, and insurtechs like Alignment Health (+31% YoY).

Health systems might prefer working with regional nonprofits and BCBS plans over their national payer rivals, but there are also fewer synergies to be had compared to a provider-sponsored MA plan. The hard financial reality is that many health systems can’t afford to absorb losses in the current environment regardless of strategic utility, and most health system-sponsored MA plans lack the scale to overcome their fixed costs and make margin.

3. The exclusion of chart reviews from risk scoring will punish bad actors who gamed the system, but mission-aligned providers will see a more limited impact

The new policy on chart reviews will have a disproportionate impact on the national for-profit payers like UnitedHealth that engaged in these tactics most aggressively. Rebalancing reimbursement away from these bad actors could create an opening for mission-aligned nonprofit and provider-sponsored plans that were more likely to pair chart reviews with appropriate follow-up care.

This divide is already apparent among industry lobbyists: AHIP (which includes for-profits in its membership) has sharply pushed back against the proposal, while the Alliance of Community Health Plans (solely representing nonprofits) called the change a “welcome step” despite disappointment in the overall level of reimbursement.

4. MA payers might be tempted to engage in more aggressive utilization management, but they’re also facing political and regulatory pressure not to.

As reimbursement headwinds intensify, MA plans are likely to revisit prior authorization, medical necessity criteria, and other utilization controls to protect margins. At the same time, increased regulatory oversight, public scrutiny, and bipartisan concern over access and denial practices materially limit the extent to which plans can pursue these strategies without backlash.

Health systems can exploit this dynamic by taking contract disputes public, using media attention and regulatory scrutiny to pressure MA payers. Framing negotiations around patient access, care disruption, and community impact can materially shift leverage in ways that private, bilateral discussions often cannot.