After initially proposing an effectively flat MA rate increase in January, CMS reversed course and instead finalized a 2.48% increase. Stock prices for carriers like UnitedHealth Group and Humana surged by roughly 10% on the news, and overall MA payments are now expected to increase by more than $13B next year.

The rate increase follows a familiar pattern of rate bumps between CMS’s initial proposal and the finalized rates. Payers, provider groups, and advocacy organizations flooded the agency with a record-breaking 47K public comments highlighting potential impacts on benefits and network adequacy. Lobbying groups also mobilized beneficiaries to write letters and make phone calls, funded research, and ran targeted ads on social media and popular streaming platforms.

A few days before the rate announcement, CMS also finalized an overhaul of the MA star ratings system that cuts several metrics used to judge plans and reverts to a previous, more generous bonus system.

So What?

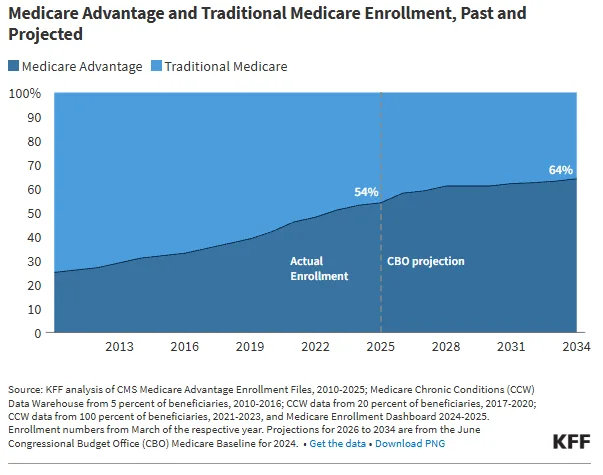

1. MA payers won this round, but the reprieve might only be temporary.

A key decision behind the rate increase is CMS’s decision to delay an update to its risk adjustment model—keeping their model calibrated on older data (2018 diagnoses and 2019 expenditures). But Medicare Director Chris Klomp said the agency is “not throwing the risk adjustment model out,” and left the door open for future changes.

The upward adjustment showcases the MA lobby’s political clout, especially in a midterm election year when policymakers are particularly sensitive to the needs of seniors (a reliable voting bloc). But even those efforts have their limit, and it’s still likely that MA will face further financial pressures in future updates given the conventional wisdom backed by a recent MedPAC analysis that the program’s costs are disproportionately high relative to traditional Medicare once you adjust for the health status of enrollees.

2. Higher rates might mean more generous benefits, and less aggressive utilization management.

In our previous analysis of the proposed flat rate increase, we speculated that financial pressures could push payers to continue engaging in aggressive utilization management. With those pressures alleviated somewhat, such moves might be less necessary.

Payers are cognizant that tactics like widespread prior authorization have attracted the ire of the public and policymakers and are taking steps to clean up their image. For example, AHIP and the Blue Cross Blue Shield Association recently boasted about an 11% reduction in prior auth requests based on a survey of insurers. For health systems, these efforts might reduce the clinical and administrative burdens of prior authorization on the margin, though we wouldn’t say it’s exactly a game changer at this point.

While the boosted MA rates provide payers some relief, MA carriers are still facing greater financial pressure than they did a few years ago. It’s possible they’ll redirect some of their cost-cutting energy towards more aggressive contract negotiations with health systems, where blame can be more evenly shared between payers and providers. And regardless of the generosity of CMS’s rates, it’s worth keeping in mind that payers are always engaged in a race to the bottom to cut care costs so that they can entice enrollees with lower premiums and capture market share.

3. The Trump administration might find other ways to funnel enrollees into MA.

The program’s reduced generosity in recent years has pushed carriers to eliminate many supplemental benefits that enticed enrollees to pick the program over traditional Medicare, but policymakers might find other avenues to continue boosting the share of enrollees in MA.

Rep. David Schweikert (R-Ariz.) introduced a bill last year that would automatically enroll new beneficiaries in the lowest-premium MA plan unless they actively opt out, and Medicare Director Chris Klomp said the agency would explore similar proposals to enroll beneficiaries in MA plans or ACOs at a STAT News summit in March.

Slowing enrollment growth fueled some speculation that MA’s share of beneficiaries might plateau, but policy tweaks could keep that number marching upwards, ultimately impacting the payer mix that health systems face.

4. The star ratings system will refocus on metrics that provider-sponsored plans already excel at, but it also could open the door to more payer misbehavior.

CMS’s changes to the star ratings system removes metrics related to administrative processes (call-center performance, appeals timeliness, provider complaints) and also scraps a Biden-era Health Equity Index. Instead, the ratings system will double down on traditional quality metrics like clinical outcomes, medication adherence, and patient experience.

Already, 86% of members in provider-sponsored plans (PSHPs) were in a 4+ star plan eligible for bonuses, reflecting providers’ greater capability to directly influence and monitor clinical quality measures. Given their existing track record, it’s reasonable to assume that PSHPs will continue their recent strong performance on these core metrics.

The trade-off for health systems is that CMS also removed star ratings measures related to appeals timeliness and appeals outcomes—metrics that had created at least some ratings-linked incentive for plans to handle coverage disputes fairly. Without that pressure, plans face fewer consequences for aggressive denial practices. That's a real concern: a 2018 HHS OIG report found that MA plans were overturning 75% of their own denials on appeal, suggesting that many initial denials weren't clinically warranted in the first place.