Table of Contents

Insights from The Health Management Academy's Virtual Forums

The Health Management Academy’s summer Virtual Forums reveal market intelligence and frontline action plans on how health system executives are responding to declining margins, coverage policy changes, and site-neutral payment expansion. These converging pressures are forcing a fundamental shift in growth strategy. The result is a strategic imperative: asset-light growth that prioritizes operational efficiency and optimized care delivery sites.

Key Takeaways for Health System Leaders

Redefine growth for a resource constrained era: Move from physical expansion to productivity expansion.

Treat AI as a scale enabler: Prioritize use cases that demonstrably improve access, throughput, and workforce satisfaction.

Make site neutrality a catalyst, not a constraint: Use policy pressure as a forcing function to optimize care models and outmaneuver competitors.

Design with affordability in mind: Even if not top of mind today, affordability will shape tomorrow’s growth, partnerships, and payer negotiations.

Margin Recovery Is Reversing—Capital Scarcity Will Shape Strategy

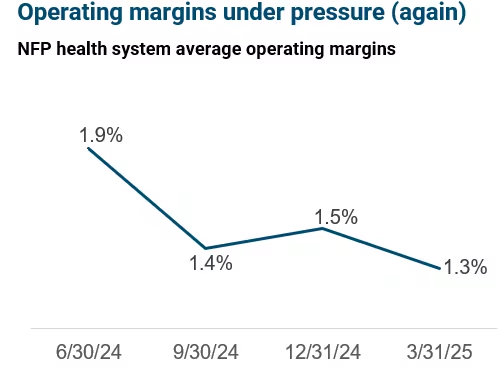

Recent gains in hospital margins have faltered, with aggregate margins for not-for-profit health systems falling to 1.3% in Q1 2025—down from 1.9% just three quarters ago.

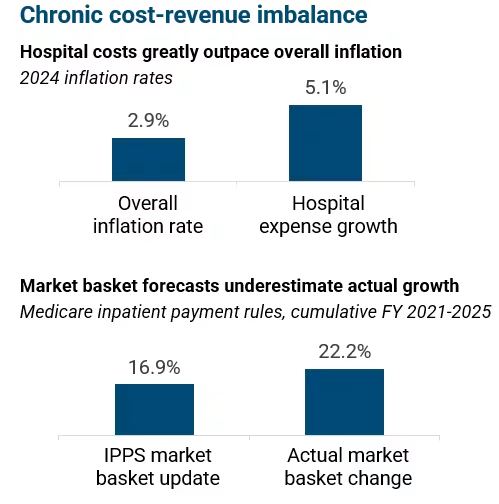

Despite differences in credit rating, even highly rated systems are experiencing cost growth that exceeds revenue gains.

Key driver: Hospital expenses are rising at nearly twice the rate of general inflation—particularly labor costs.

Strategic imperative: Systems must plan for lower capital availability and heightened scrutiny on ROI for any new investment, making efficiency and scalability paramount.

Policy Shifts Are Shrinking Coverage and Reshaping Growth Potential

The recently passed federal reconciliation bill is expected to result in more than 10 million more uninsured by 2034 due to Medicaid and ACA coverage cuts.

Policy changes create a triple threat to traditional health system economics

Access disruption: Higher uninsured loads will strain capacity while reducing revenue

Revenue erosion: Loss of Medicaid reimbursements, potential loss of 340B eligibility, and reduced supplemental payments

Cost amplification: Increased administrative burden, higher case acuity, and potential post-acute care bottlenecks

$1T

in Medicaid federal cuts

$10M+

More uninsured expected by 2034

Additional pressure comes from proposed expansions in site-neutral payment and a phase out of the inpatient-only list, which could flatten reimbursement across settings and favor more cost-efficient competitors.

Strategic imperative: Health systems must prepare to do more with less while facing increased demand for uncompensated care and downward pressure on outpatient revenue.

Operational Scale: Turn Internal Efficiency into Growth Capacity

Systems are turning to AI and automation to boost productivity, enhance clinical capacity, and support care teams—without expanding facilities.

A $5B system could unlock $190M+ in new revenue by leveraging AI for documentation support, OR optimization, and patient flow improvements.

AI applications are already producing results:

Montefiore: 36% higher colonoscopy volume through AI-powered navigation

Geisinger: AI scheduling unlocked 185 additional OR hours monthly

Strategic imperative: AI and automation are now essential infrastructure for scale—leaders must prioritize investments that expand clinical and operational capacity at low marginal cost.

Site-of-Service Strategy: Cost-Aware Growth Starts with Where You Deliver Care

The combination of site-neutral payment expansion, rising consumer expectations, and competitive threats from for-profit ASC operators make location strategy more urgent.

Systems need to align affordability and growth goals by shifting care to lower-cost settings—without losing market share or diluting value.

Systems that use this disruption as a catalyst for fundamental care delivery reimagination will outperform those focused solely on cost management

Most health systems are in the early stages of ambulatory surgery center (ASC) strategy. Meanwhile, operators for-profit operators like HCA target 600 ASCs in 2025.

The leading edge is not just building ASCs—but integrating them into network-wide strategies with tailored models, aligned physician incentives, and purpose-built infrastructure.

Strategic imperative: Site strategy is becoming a strategic differentiator. Success will hinge on balancing systemness and regional customization, disciplined scaling to avoid capital strain and operational efficiency and readiness for reimbursement disruption.

Health System Leaders Identify 5 Priority Initiatives

Strategic Timing of Site Migration: Carefully sequence the movement of services from hospital outpatient departments to lower-cost settings while ensuring adequate volume backfill to protect hospital margins and avoid revenue cannibalization.

Ambulatory Infrastructure Assessment: Conduct comprehensive capacity evaluations across outpatient services and medical groups to identify underutilized assets and gaps in ambulatory planning and readiness.

Proactive Payer Mix Management: Implement assertive financial strategies including scheduling algorithms, enhanced eligibility verification, and payment model optimization to ensure full capture of insured patients and to manage uncompensated care exposure.

Point-of-Care Financial Triage: Deploy scheduling systems, real-time eligibility checks, and prepayment models to manage financial risk and optimize payer mix at the time of care delivery – especially for elective services.

Operationally-Aligned AI Implementation: To unlock the value of AI solutions, focus adoption on process redesign and cultural readiness rather than technology alone, ensuring physician engagement and operational ownership for tools like bed management and patient flow optimization.