By nature, health systems are compelled to pursue adoption of clinical innovations to improve care delivery and health outcomes. But the resource-intensive nature of adopting clinical innovations means that health systems can’t pursue everything. Therefore, many are taking a measured approach towards investment, with a focus on alignment with strategic goals. Based on a 2023 survey of 30 unique Leading Health System executives involved in clinical innovation strategy and decision making we learned the following insights:

Investments in clinical innovations are driven by their potential to drive growth

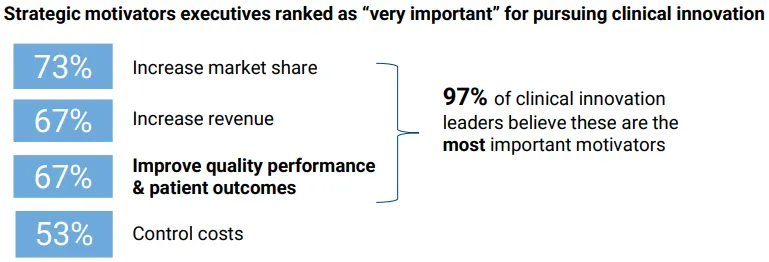

By nature, health systems are compelled to adopt clinical innovations that can meaningfully improve care delivery and health outcomes. But tight financial circumstances and the significant costs involved means there is an increased pressure to focus on innovations that enable long term financial growth by growing their market share and increasing revenue in addition to improving quality and health outcomes. Therefore, health systems will likely focus on innovations that enable their strategic motivators (e.g., market differentiation, revenue growth, etc.) or align with a broader organizational strategy (e.g., value-based care, health equity, etc.)

Directed service line growth is driving investment decisions

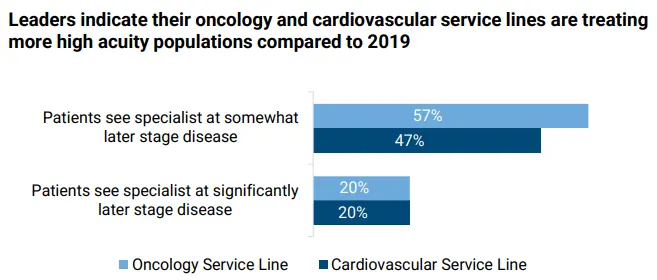

Cardiovascular, oncology, and neurology service lines were overwhelmingly ranked as the top business units health systems are prioritizing for growth, meaning they will have a stronger business case for innovations (e.g., gene therapy, genomic testing, advanced immunotherapy) that improve care delivery for these service lines. Another interesting data point was that health systems are also seeing more oncology and cardiovascular patients with a higher acuity, which may be indicative of higher volumes for AMCs and health systems providing secondary and tertiary care but could pose challenges for health systems focused on value-based care and looking to invest in early stage/preventative care (e.g., genomic testing, pharmacogenomics).

Leaders are looking for clinical innovations with clear use cases and strong potential to enable growth

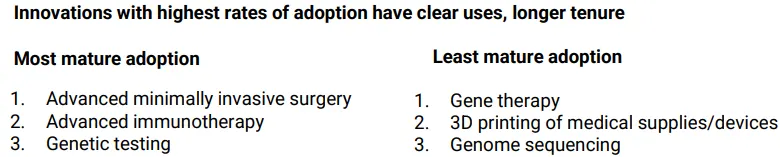

Conviction on immediate impact is reserved for more mature innovations, but AI’s myriad of use cases supersedes its lack of mature adoption.

Leaders indicated the highest confidence in the most broadly adopted innovations, (e.g., advanced minimally invasive surgery, advanced immunotherapy, and genetic testing), because of their clear use cases, ability to enable growth strategies (e.g., ambulatory and service line growth), and fewer risks. Clinical applications of AI is a notable exception, where its substantial use cases and potential to enable growth and contain costs has leaders confident in its impact despite its nascent use in healthcare delivery. Conversely, 70% of clinical leaders on average stated they were “neutral” or only “somewhat convinced” about the overall impact of less commonly adopted innovations like gene therapy, 3D printing of medical supplies/devices, and genome sequencing which have fewer use cases than AI and less mature industry adoption than advanced minimally invasive surgery.

Key Takeaways on How Health Systems are Investing in Clinical Innovation

The motivators driving innovation are primarily financial, with 73% of leaders saying growing market share is their most important strategic motivator. Therefore, health systems will likely continue to focus on innovations such as advanced minimally invasive surgery, advanced immunotherapy, and genetic testing as they support broader strategies for growing market share and revenue (e.g., capturing new patients, service line growth).

Service line growth decisions are guiding investment strategy. Leaders reported that they are prioritizing cardiovascular, oncology, and neurology service lines. Therefore, their investment decisions are tied to innovations supporting these service lines like gene therapy, genomic testing, and advanced immunotherapy. All of these investments are important as these service lines are seeing patients needing higher acuity care compared to five years ago. To keep cost-per-case under control, many are trying to pursue innovations focused on earlier detection and preventative care.

There is little desire to invest in unproven innovations—except AI. Leaders indicated the highest confidence in investing in the most broadly adopted innovations (e.g., advanced minimally invasive surgery), because of their clear use cases, ability to enable growth strategies, and fewer risks. Clinical applications of AI were a notable exception. AI’s substantial use cases and potential to contain costs has leaders confident in its impact despite its nascent use in healthcare delivery. Conversely, 70% of clinical leaders on average stated they were “neutral” or only “somewhat convinced” about the overall impact of less commonly adopted innovations like 3D printing of medical supplies/devices, gene therapy and genome sequencing.