Section Summary

Health system strategy, operations, and service line leaders from across the U.S. assessed 14 service lines and evaluated each on its role in the system, margin performance, mission importance, and current strategic posture. What emerged is a consistent gap between how leaders say they value service lines and what actually drives the decisions they make about them. We call this the Valuation Paradox.

This section is from Strategy Catalyst's report—Service Line Portfolio Strategy in 2026: Where Health Systems Are Growing; How They Are Rationalizing; and What Leaders Regret The Most. Access survey insights on the executive summary page.

Key Section I Findings

Finding 1: Stated values vs. actual decisions

Health system leaders broadly agree that quality, margin, and mission are all critical when evaluating a service line. However, the factors that actually trigger portfolio changes—expansion, divestiture, or partnership—are mostly financial.

Finding 2: Mission vs. margin

Health systems are expanding lines that are classified as strong and weak margin contributors, even as margins for some mission-anchored services decline. No system has fully exited a service line in the past two years, signaling that mission carries real strategic weight.

Survey Questions Covered in This Section:

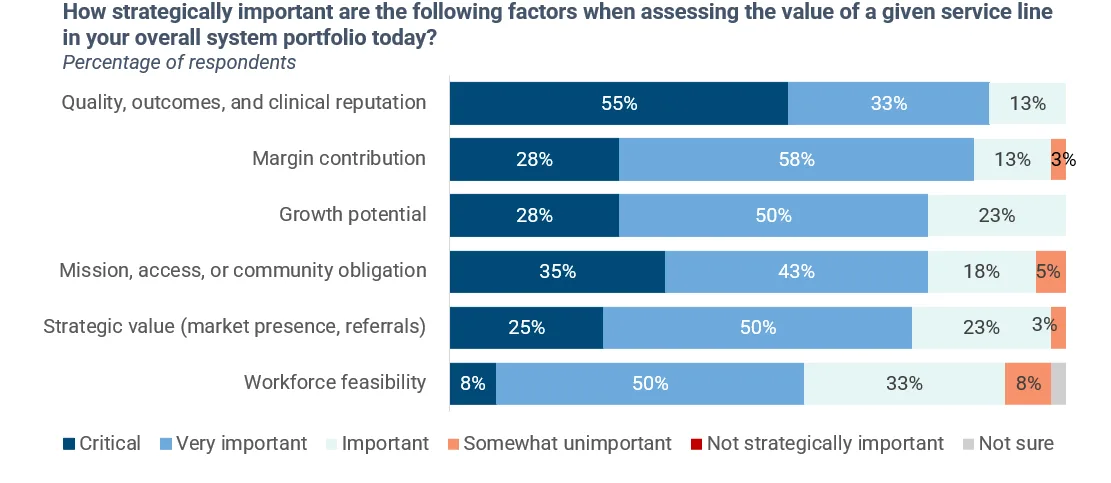

How strategically important are the following factors—margin contribution, growth potential, mission/access/community obligation, quality/clinical reputation, workforce feasibility, strategic value—when assessing the value of a given service line in your overall system portfolio?

Which factors most influence enterprise-level service line portfolio decisions?

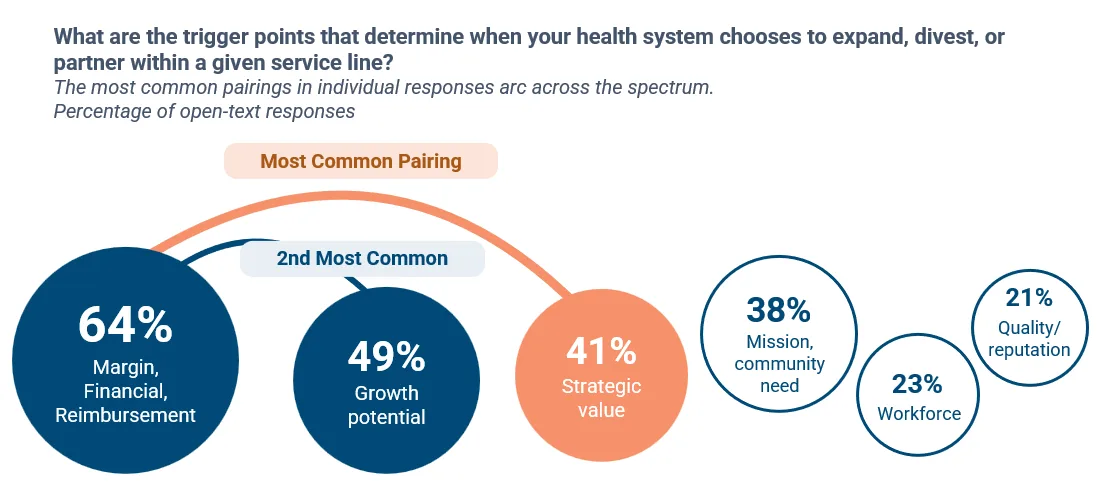

What are the trigger points that determine when your health system chooses to expand, divest, or partner within a given service line?

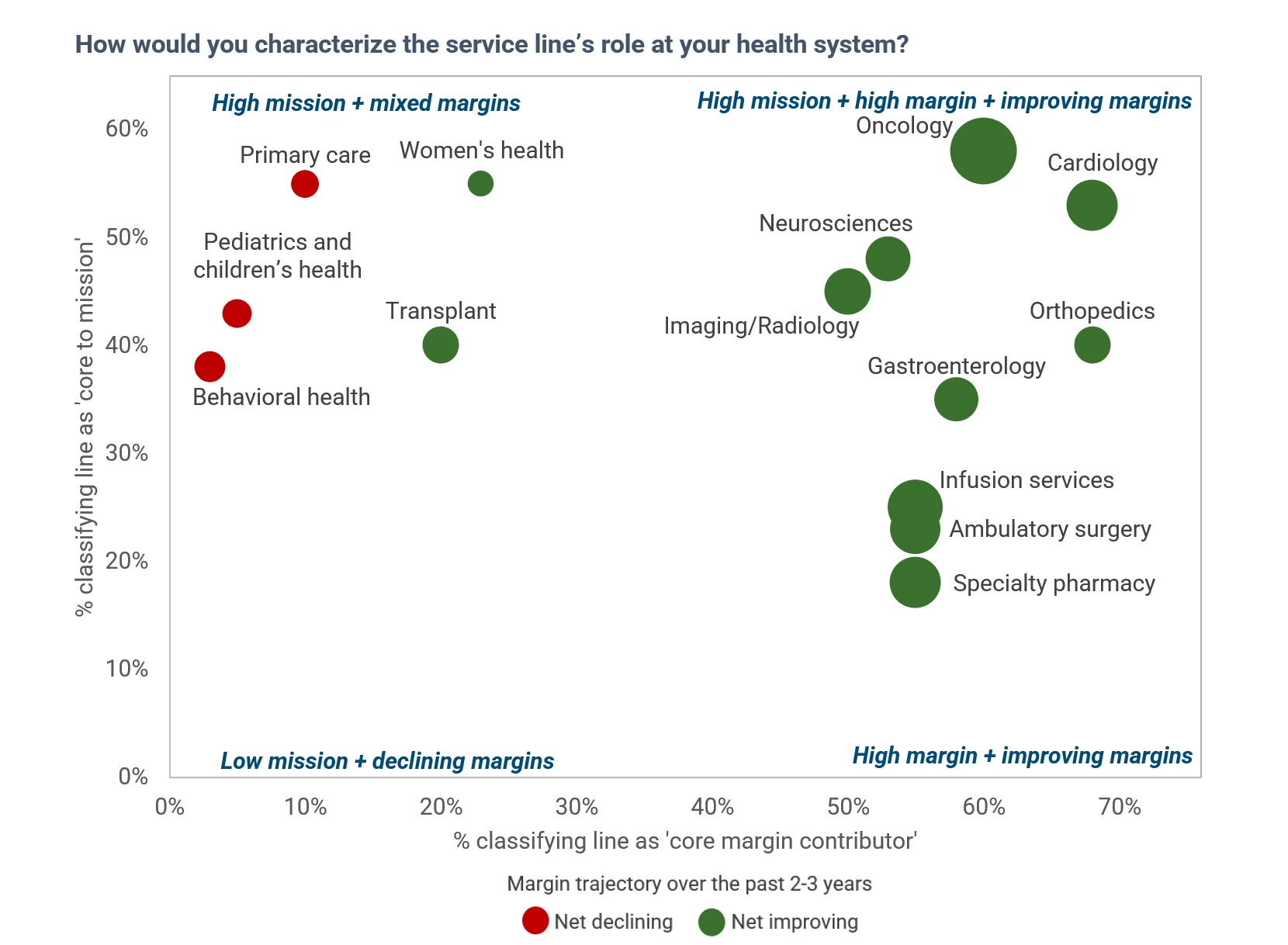

How would you characterize the service line’s role at your health system: core to mission, core margin contributor, strategically important but financially volatile, at risk/break even, structurally margin negative?

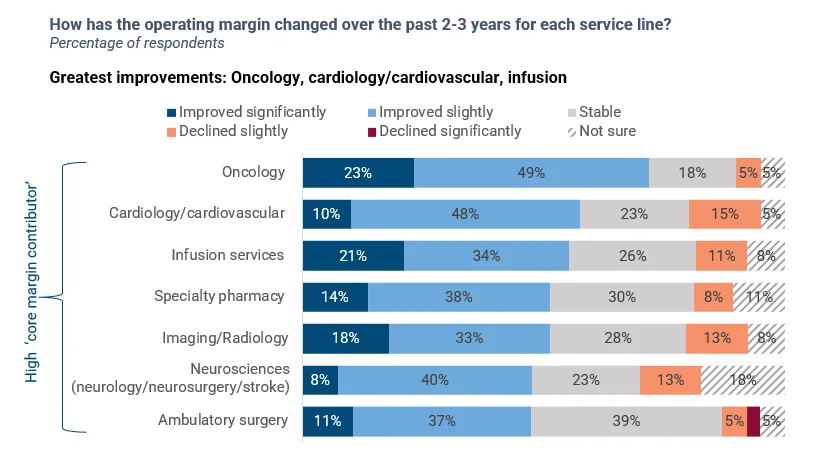

How has the operating margin changed over the past 2-3 years for each service line?

What are the strategic shifts underway within each service line: actively expanding, partnering/JV, consolidating locations, shifting site of care, reducing service scope, no material change, preparing to exit, exited within the last 24 months?

Finding 1: Leaders say mission, quality, and margin matter equally; financial signals are what drive service line decisions in practice.

Stated values are balanced. Decision drivers are not.

Three-quarters or more rated five of six strategic factors as “very important” or “critical.”

Comparing that to the question about what most influences portfolio decisions, payer mix and reimbursement sustainability top the list. Quality still makes the top 5 but drops to 33%. At the abstract valuation level, mission and quality sit alongside margin in the top tier of importance. At the execution level, portfolio decisions are based almost entirely in financial and market signals.

Portfolio decisions are a joint test of service line finances and strategic role

While there is no single trigger that leads health systems to expand, divest, or partner within a given service line, margin contribution and strategic value (e.g., market presence, downstream revenue, referral capture) appeared most frequently together in responses.

So what?

Mission obligations are non-negotiable for most non-profit systems, meaning mission-critical lines are rarely exited for financial reasons. Therefore, the question is never whether to cross-subsidize mission lines but whether the governance infrastructure exists to do it sustainably.

Service lines whose value rests on margin or market signals are well-served by current decision machinery. Service lines whose value rests primarily on mission or quality are not.

Portfolio discipline on mission-anchored lines must be intentionally built. The finding that systems might 'value’ a service line because of mission or quality while still making business decisions based on margin is not necessarily a contradiction. However, health systems should consider:

Aligning stated valuation to actions or building the governance mechanisms to incorporate quality and mission in capital decisions.

Clearly naming where the organization will not achieve positive margin or invest, rather than continuing to signal priorities that aren’t meaningfully supported by financial, strategic, or operational focus.

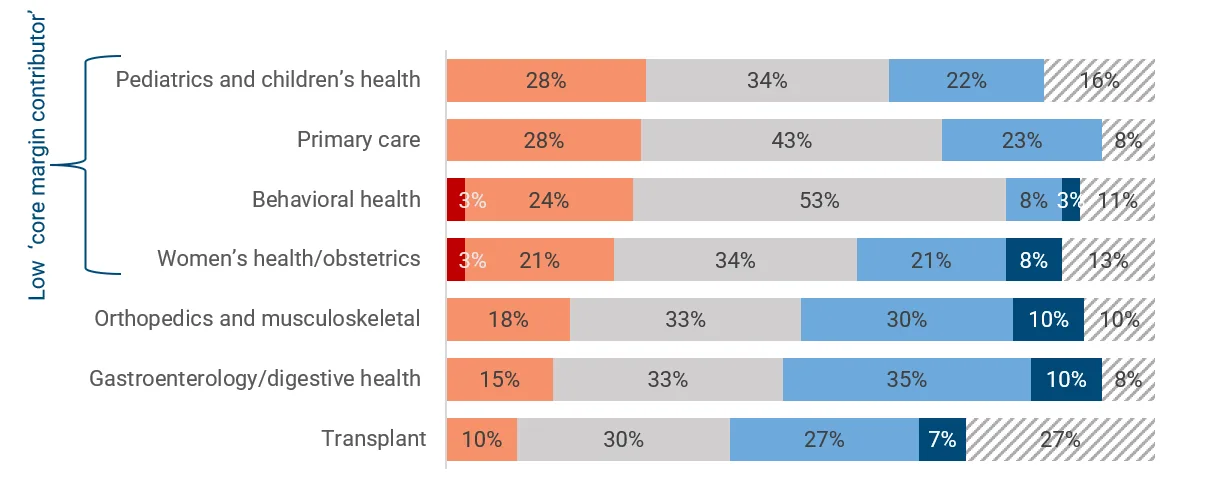

Finding 2: Margin classification is a stronger indicator of margin trajectory than mission classification. That being said, systems are broadly expanding service lines, including some with lower margins.

Oncology and cardiology are key high-mission lines with strong margin performance. Primary care and pediatrics are high-mission lines with negative margin trajectory.

A subset of service lines strongly identified as 'core to mission' but not strongly identified as 'core margin contributors' are losing financial ground.

Greatest improvements: Oncology, cardiology/cardiovascular, infusion

Greatest declines: Pediatrics and children’s health, primary care, behavioral health. These mission-anchored lines are, at best, drifting towards stability.

Most systems are broadly expanding service lines. No system surveyed has exited a service line within the past 2 years, with portfolio adjustment favoring partnerships and consolidation over exits.

7 in 10 systems continue to expand primary care despite margin pressure.

Health systems are most likely to partner/pursue JVs for ambulatory surgery.

Specialty pharmacy shows the highest stability in terms of strategic shifts underway. High financial performers like specialty pharmacy are likely to hold course or expand.

Behavioral health is sustained for mission-driven reasons.

So what?

The valuation paradox raises a hard question: what, if anything, should trigger a formal review of portfolio decisions for service lines that are losing financial ground?

Behavioral health is the one mission-anchored line where financial pressure has begun to slow growth—yet notably, most health systems have not exited. Instead, they are consolidating and deepening partnerships, signaling that mission commitment remains a floor even under strain.

For primary care—and to a lesser extent pediatrics—continued growth against a negative financial trend points to the role of indirect and downstream revenue. These lines function as system entry points whose value is not fully captured in their own margins.